CALL US NOW

CALL US NOW EMAIL US NOW

EMAIL US NOW

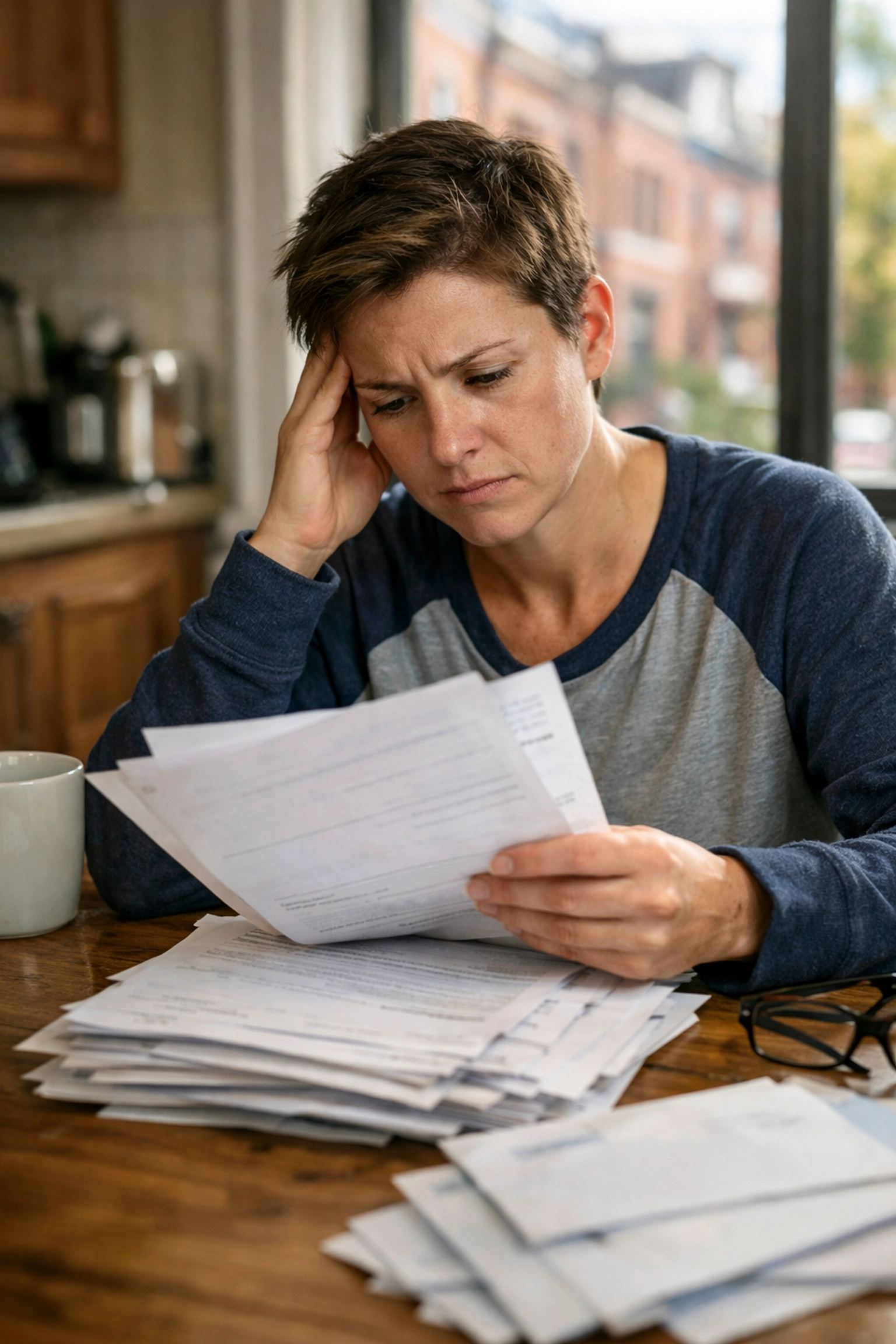

You just survived a car accident in Boston. Your heart is racing, your neck is stiff, and your car is a wreck. In the days following the crash, the adrenaline wears off and reality sets in. Then, the mail starts arriving. Medical bills from the ER, the ambulance company, and the radiologist begin to pile up. It is an incredibly stressful time. You are likely sitting at your kitchen table wondering, who pays medical bills in a car accident?

In Massachusetts, we operate under a “no-fault” insurance system. This sounds like it should make things simple. It suggests that your own insurance company just handles everything regardless of who caused the crash. Unfortunately, the system is rarely that straightforward. Between confusing PIP limits and insurance company delays, getting your bills paid can feel like a second full-time job.

At Joel H. Schwartz, P.C., we have spent over 60 years helping victims navigate this exact mess. We have handled more than 30,000 claims. We know how the insurance companies play this game. Here is the truth about medical bills and why your standard coverage often falls short.

Understanding Personal Injury Protection (PIP)

The first thing you need to know about who pays medical bills in a car accident is Personal Injury Protection, or PIP. Massachusetts law requires every auto policy to have at least $8,000 in PIP coverage.

In theory, PIP is designed to get your medical bills paid quickly. You don’t have to wait for a court to decide who was at fault. However, the amount of PIP available to you depends heavily on whether you have private health insurance.

If you have health insurance, PIP typically only covers the first $2,000 of your medical bills. After that, your medical providers must submit the bills to your health insurance company. If you do not have health insurance, PIP may cover up to the full $8,000.

The 75% Income Trap

PIP isn’t just for doctors. It is also supposed to cover your lost wages if you can’t work. But here is the catch: PIP only covers 75% of your average weekly gross income. If you are already struggling with medical costs, losing 25% of your paycheck is a massive blow. We see this happen constantly. A client is out of work for three weeks, and suddenly they can’t make their mortgage payment because PIP didn’t cover their full salary.

Why PIP Frequently Isn’t Enough

The $8,000 limit was set decades ago. In 2026, medical costs have skyrocketed. A single trip to a Boston emergency room, an MRI, and a few weeks of physical therapy can easily blow past $8,000.

Here are the three main reasons PIP usually leaves victims hanging:

- The $2,000 Deductible/Health Insurance Coordination: As mentioned, if you have private health insurance, PIP stops paying at $2,000. Your health insurer then takes over, but they often have high deductibles and co-pays. You might end up paying thousands out of pocket before your health insurance even kicks in.

- Serious Injury Costs: If you suffer a broken bone, a concussion, or a spinal injury, $8,000 is a drop in the bucket. If your injuries happened while walking or crossing the street, our Pedestrian Accident Guide can help you understand how serious injuries affect these claims. For more information on the impact of head injuries, you might want to read our newsletter on kids and concussions.

- Insurance Company Delays: Even though it’s called “no-fault,” insurance companies aren’t always eager to pay. They may delay payments by requesting “independent” medical exams or questioning whether your treatment was reasonable and necessary.

Crossing the Threshold: Filing a Claim Against the At-Fault Driver

Since PIP often falls short, you need to know when you can step outside the no-fault system. In Massachusetts, you can sue the at-fault driver for additional damages: including pain and suffering: if you meet certain “tort thresholds.” You must meet one of the following criteria:

You can generally pursue a personal injury claim if:

- Your reasonable medical expenses exceed $2,000.

- You suffered a permanent and serious disfigurement.

- You suffered a fractured bone.

- The accident resulted in a loss of sight or hearing.

When you cross this threshold, you aren’t limited to the tiny PIP bucket. You can go after the at-fault driver’s bodily injury liability coverage. This is where we step in. We fight to make sure the person who caused the accident: and their insurance company: pays for the full extent of your damages, not just the bare minimum.

The Injured Victim’s Bill of Rights

When you are hurt in an accident, you have rights that insurance adjusters won’t always tell you about. At Joel H. Schwartz, P.C., we believe every victim should know where they stand.

- The Right to Choose Your Doctor: You are not required to see a doctor chosen by the insurance company for your primary treatment.

- The Right to Full PIP Benefits: You are entitled to up to $8,000 (depending on your health insurance) for medical bills and lost wages.

- The Right to Compensation for Pain and Suffering: If your injuries are serious or your bills exceed $2,000, you have the right to seek money for the physical and emotional toll of the crash.

- The Right to Legal Counsel: You have the right to hire an attorney to handle the insurance company for you.

- The Right to a Contingency Fee: You should never have to pay a lawyer upfront. We only get paid if we win your case.

Why Experience Matters When Dealing with Insurance Companies

Insurance companies are billion-dollar corporations. Their goal is to pay out as little as possible. They use sophisticated software and aggressive adjusters to minimize your claim. If you are handling this on your own, you are at a disadvantage.

We have handled over 30,000 claims. We have seen every trick in the book. Whether it’s a case involving distracted driving or a crash where sharing the road is a key issue, our Bicycle Accident Guide shows how these cases often turn on visibility, lane use, and driver awareness. We know how to build a case that forces the insurance company to take you seriously.

According to the Official Massachusetts Government Website, there are very specific rules regarding how insurance policies must be written and how claims must be handled. We hold insurers accountable to these laws every single day.

Why Choose Joel H. Schwartz, P.C.?

There are a lot of law firms out there. You see them on billboards and hear them on the radio. But there is a reason we have been a staple in the Boston legal community for over six decades.

60+ Years of History

We aren’t a “here today, gone tomorrow” firm. We have been helping injured people in Massachusetts for over 60 years. Our deep roots in the community mean we know the local courts, the local doctors, and the local defense attorneys.

$500 Million Recovered

Results matter. We have recovered over $500 million for our clients. That money has helped families pay off medical debt, replace lost income, and rebuild their lives after devastating accidents.

30,000+ Claims Handled

Every accident is unique, but after 30,000 claims, there isn’t much we haven’t seen. We understand the nuances of comparative negligence and how it affects your payout. This experience allows us to anticipate insurance company moves before they even make them.

Our Awards and Accolades

We don’t just say we are the best; the legal community recognizes our hard work and dedication to our clients.

- The National Trial Lawyers Top 100: Our attorneys are recognized among the elite trial lawyers in the country.

- AV Preeminent Rated: This is the highest possible rating for both legal ability and ethical standards.

- Avvo Rating 10/10 Superb: We maintain a perfect rating based on client reviews and professional milestones.

- BBB A+ Rating: We pride ourselves on transparent, honest communication with every person who walks through our doors.

What Should You Do Right Now?

If you are worried about who pays medical bills in a car accident, don’t wait for the insurance company to make the first move. They are already working to protect their bottom line. You need someone working to protect yours.

- Seek Medical Attention: Even if you feel “fine,” many injuries like whiplash or internal trauma don’t show symptoms immediately.

- Don’t Give a Recorded Statement: The insurance adjuster for the other driver will call you. They may sound friendly, but they are looking for reasons to deny your claim.

- Document Everything: Keep copies of every medical bill, every prescription receipt, and every letter from the insurance company.

- Call a Professional: You have enough on your plate. Let us handle the paperwork and the phone calls.

Remember, at Joel H. Schwartz, P.C., we work on a contingency fee basis. This means you don’t pay us a dime unless we win your case. There is no risk to you.

Contact Joel H. Schwartz, P.C. Today

The truth is that PIP is rarely enough to cover the true cost of a Boston car accident. Between rising medical costs and the 25% gap in lost wages, many victims find themselves in a financial hole they can’t climb out of alone.

We are here to help you get the full compensation you deserve. Whether your accident was caused by drowsy driving or someone eating while driving, you shouldn’t have to pay for someone else’s mistake.

Visit our website at joelhschwartz.com to learn more about your rights, or give us a call for a free, no-obligation consultation. We have the experience, the resources, and the track record to fight for you. Let’s get you back on your feet.